Collectibles vs Investments: Which Belongs in Your Financial Plan?

In recent years, we have been having more conversations with clients regarding collectibles and how those could work into their financial plans. Previously, we normally would come across a collection of stamps, firearms, or vintage automobiles.

Most of the collections on our financial plans were rather modest and were never the main wealth generator for the client. They were simply a hobby that they had been partaking in for decades and have accumulated a decent amount over time.

What Are Collectibles and Why the Recent Surge in Interest?

Since the COVID pandemic of 2020, we have seen an emergence of interest in collectibles whether it be silver or gold, fine art or furniture, toys or video games, or the popular trend of sports and Pokémon cards. We are not sure of the initial root cause of this, but our assumption is that people had more time on their hands to look into collectibles during the COVID lockdown.

Plus, the government assistance that was provided possibly gave some extra discretionary cash that could be spent on these new interests. Some have likely started collecting simply as a hobby while others are chasing a big score, which could be driven by social media influencers who post about their collections.

For example, Logan Paul recently sold a Pokémon card for $16 million, which tripled his cost basis in just a handful of years (www.cnbc.com).

Why Are People Drawn to Collectibles?

There have been times when our clients/prospects actually have more of their net worth allocated to various collectibles rather than more traditional investments and the frequency of collections seems to be increasing, especially among our younger clientele. I believe this increase in interest is partially driven by social media influencers who have convinced others to join the trend.

However, the increase in collectibles could also be due to the ability to hold and physically obtain the collectibles. Some of my conversations with clients and prospects have confirmed that they prefer to allocate their resources to collectibles because it is something tangible rather than an investment portfolio that simply shows a dollar value on the screen.

This physical nature could increase the emotional connection to the collection and it is very easy to understand, while the stock market and traditional investments require a higher level of financial literacy.

Collectors, even if not at first, tend to become very knowledgeable about their collection and this can cause them to become comfortable with owning more and more of that type of asset. These are a couple of possible examples of why clients may have a strong passion to accumulate a collection and this passion could be the main reason why people start and continue collecting (www.ubs.com).

How Do Collectibles Compare to Traditional Investments?

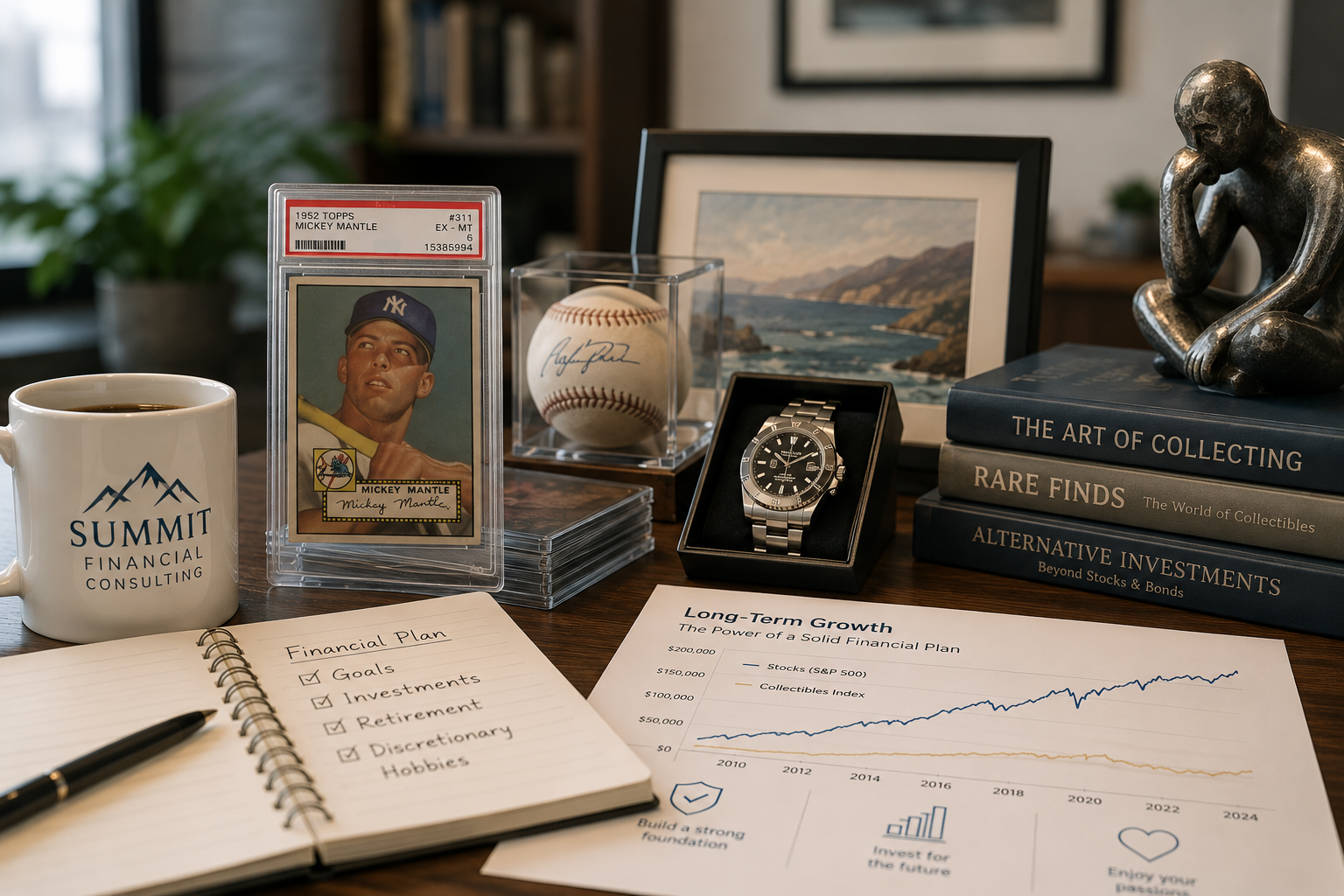

While collectibles may seem more exciting due to the emotional connection, we believe only discretionary resources should be spent on collections since the long-term growth can be difficult to accurately forecast. If a client has a strong financial plan, we are comfortable with them allocating resources to their collection as a hobby. Our main concern is when the hobby turns into a get-rich-quick plan and they hope to find the next big sale.

At this point, collecting could be viewed as gambling. We believe opening a pack of cards in the hopes of pulling something ultra rare is similar to scratching a lottery ticket and hoping for a jackpot.

Just like any other form of gambling, we strongly believe that more traditional investments, such as stocks or bonds, are better for a long-term financial plan.

Collectibles are normally categorized as "alternative" investments and could be useful as a hedge against inflation (www.investopedia.com).

However, it is rare that someone can actually generate a large amount of wealth from their collection and it takes a large amount of risk in order to do so. We believe on average, most collections lag most stock market indices since really the only select ultra rare items may generate a large return. This is why we stress that collecting can be a fun hobby for clients once they have established a strong financial foundation and have excess resources to allocate to the hobby.

Should Collectibles Be Part of Your Financial Plan?

The key principle is this: collectibles should only be part of your financial plan if they are paid for with discretionary resources—money you can afford to lose without affecting your long-term financial goals. If you have a strong foundation of traditional investments (stocks, bonds, retirement accounts), then collecting can be an enjoyable hobby.

However, if you're considering collectibles as a wealth-building strategy or investment vehicle, we caution against it. The returns are unpredictable, the risk is high, and most collectors do not outperform traditional investment indices. Treating collectibles like lottery tickets (hoping for the ultra-rare find) is essentially gambling, not investing.

The healthiest approach is to establish your financial plan first with traditional investments, then use only excess discretionary income for collecting as a hobby you enjoy.

Collectibles vs Investments - Key Takeaways

- Collectibles interest has surged since COVID due to increased leisure time, government stimulus, social media influence, and the tangible nature of physical assets—but this doesn't make them reliable investments.

- Collectibles appeal emotionally because they're physical, understandable, and create stronger personal connections than abstract investment portfolios—but emotional appeal doesn't equal investment performance.

- Collectibles are "alternative" investments that rarely outperform traditional stock market indices; only ultra-rare items generate significant returns, making most collections underperform over time.

- Treating collectibles as a get-rich-quick strategy is essentially gambling—similar to lottery tickets or scratch-offs; only established financial plans with excess discretionary income should fund collecting as a hobby.

- Strong financial foundation first (stocks, bonds, retirement accounts), then collectibles as hobby; never the reverse. Collectibles should never replace traditional wealth-building investments.

Questions About Your Financial Plan or Investment Strategy?

If you have any questions about your investment portfolio, retirement planning, tax strategies, our 401(k) recommendation service, or other general questions, please give our office a call at (586) 226-2100.

Please feel free to suggest this blog post to a friend, family member, or co-worker. If you have had any changes to your income, job, family, health insurance, risk tolerance, or your overall financial situation, please give us a call so we can discuss it.

We hope you learned something today. If you have any feedback or suggestions, we would love to hear them.

Best Regards,

Best Regards,

Zachary A. Bachner, CFP®

with contributions by Robert L. Wink, Kenneth R. Wink, James D. Wink, and James C. Baldwin.

Zach Bachner

After graduating from Central Michigan University in 2017 with specialized degrees in Finance and Personal Financial Planning, Zachary “Zach” Bachner set himself apart by earning the CFP® designation and passing the Series 7, 63, 65 licensing exams early in his career. Zach gained valuable real-world experience with the team at Summit Financial Consulting, who treated him like family. Their guidance helped him refine his skills in practical, client-centered planning, where putting their needs first was non-negotiable. This focus on trust-building not only allowed him to cultivate strong relationships, but also allowed him to continue doing what he loves most: solving client problems through efficient financial planning strategies. Leveraging his experience, Zach now helps others navigate finances through clear, informative writing. His work has been published in major outlets like Yahoo Finance, MarketWatch, and Investment Business Daily, establishing him as a valued resource. By simplifying complex topics, Zach aims to empower everyday people to confidently pursue their financial goals