Parents often want to give their kids a financial head start but which type of account is best? We review non-qualified accounts, custodial accounts, 529 plans, and new tax-advantaged options.

When we have a client who is set up for a successful retirement, we often see that their next goal is to help their children get a head start on life financially. The client normally has some excess cash flow, and they are interested in how to set aside some savings for their kids.

There are a few different options that we typically review with the client, and then we assist them in determining which type of account may best meet their needs. This blog will summarize some of these options, including some pros and cons with each option that should be considered before making a decision.

Non-Qualified Accounts for Children

First, the most straightforward option is for the parent to open a non-qualified account in their name and simply earmark the savings for their children. In order to keep their accounts clear, we may open up a new account if they already have an existing non-qualified account, as this will keep the child’s savings separate from their own personal savings.

We believe one of the most important advantages of this account type is that the funds remain in the parent’s name and they retain full control. This is important because they can use the funds for any unexpected expenses if needed, such as medical bills or major home repairs. Also, they can ultimately decide when they believe the child should have access to the funds in the future, in case they feel they are not responsible enough when they become an adult.

One potential downside to consider is that any interest or capital gains will be taxed at the parent’s tax rat,e and the future transfer of savings may be subject to the federal gift tax laws. However, there is the potential for some tax benefits if the parent gifts their appreciated holding to their child. For example, if a child receives appreciated stock from their parent, then they would receive their cost basis, and any realized gains at the sale of the stock would be taxed to the child’s tax bracket (Charles Schwab).

Accounts Advantages:

- Funds remain in the parent’s name with full control.

- Flexibility to use the funds for unexpected expenses such as medical bills or home repairs.

- Parent decides when the child receives access.

Accounts Considerations:

- Any interest or capital gains are taxed at the parent’s rate.

- Transfers may be subject to federal gift tax rules.

- Potential benefit if appreciated assets are gifted to the child, since realized gains may then be taxed at the child’s rate (Charles Schwab).

Custodial Accounts: Assets in the Child’s Name

The next option to consider would be a custodial account in the name of the child. This account is somewhat similar to the non-qualified option above as both accounts are technically non-qualified investments. One difference is the fact that contributions into the account are considered irrevocable gifts to the child.

This means the child technically owns the account, and any funds used while they are a minor must be for their benefit. Further, any interest or capital gains would be subject to the “kiddie tax” and this means that a small portion would be tax-free, and a small portion would be taxed at the child’s tax rate, before the remainder is taxed at the parent’s rate.

However, one of the biggest disadvantages and the main reason why clients will avoid these accounts at times, is the fact that the child will receive full control of the assets when they become an adult. Some parents do not want their child to receive a large sum of money when they turn either 18 or 21 and prefer to avoid this by choosing a different account (www.investopedia.com).

Custodial Accounts Key Features:

- Contributions are irrevocable gifts to the child.

- The child legally owns the account.

- Interest and gains are subject to the “kiddie tax,” with portions taxed at both the child’s and parent’s rates.

Drawback:

- The child gains full control at adulthood (18 or 21, depending on the state). Some parents may prefer to avoid this outcome (Investopedia).

529 College Savings Plans: Education-Focused Benefits

Another option to consider, and what we believe is one of the more common solutions, is a 529 college savings plan. These accounts are specifically geared towards funding education goals, and the money can grow tax-free as long as the funds are used for education down the road.

This means that the interest or capital gains within the account may be tax-free when they are withdrawn, likely for college expenses. We discussed these accounts previously in our blog at Summit Financial Consulting.

One recent enhancement to 529 plans is that a portion of the account may be converted to Roth IRA savings if they are not used for education. We believe that some people used to be worried about choosing this account type since withdrawals would be taxed and penalized if used for non-education expenses. Still, now they can be converted to a Roth IRA instead, which may alleviate this concern.

529 Savings Plan Considerations

- Interest and gains may be withdrawn tax-free for education expenses.

- Recent changes allow a portion of unused funds to be converted to Roth IRA savings.

- Concerns over penalties for non-education withdrawals are somewhat reduced by this new flexibility (Summit Financial Consulting).

Trump Accounts: A Proposed New Option

Lastly, we felt the need to describe a new account type that is not yet available – Trump Accounts. These will soon be offered as part of the One Big Beautiful Bill that was recently passed.

These accounts will be funded at birth by the government, but then parents will have the option to fund them additionally on their own or through contributions by an employer. The money within will be invested in US equity index funds and will grow tax-deferred until the child reaches age 18. At that time, the account will convert to an Individual Retirement Account (IRA) in the name of the child.

Since the child will own this account at 18, the same concern exists for giving a lump sum of money to a new adult just like the custodial investment options.

However, one of our concerns revolves around the taxation of these accounts. Contributions from a parent will be tax-free when withdrawn, and contributions from an employer and any growth/interest in the account will be taxable when withdrawn. There could also be an additional 10% penalty if the funds are not withdrawn for a qualified expense. (www.kiplinger.com).

We believe this means that penalties or taxes could hinder the attractiveness of these accounts, while other, more tax-advantaged options may exist. More clarification is needed from the IRS before these accounts are available to determine whether funding these accounts makes sense for our clients.

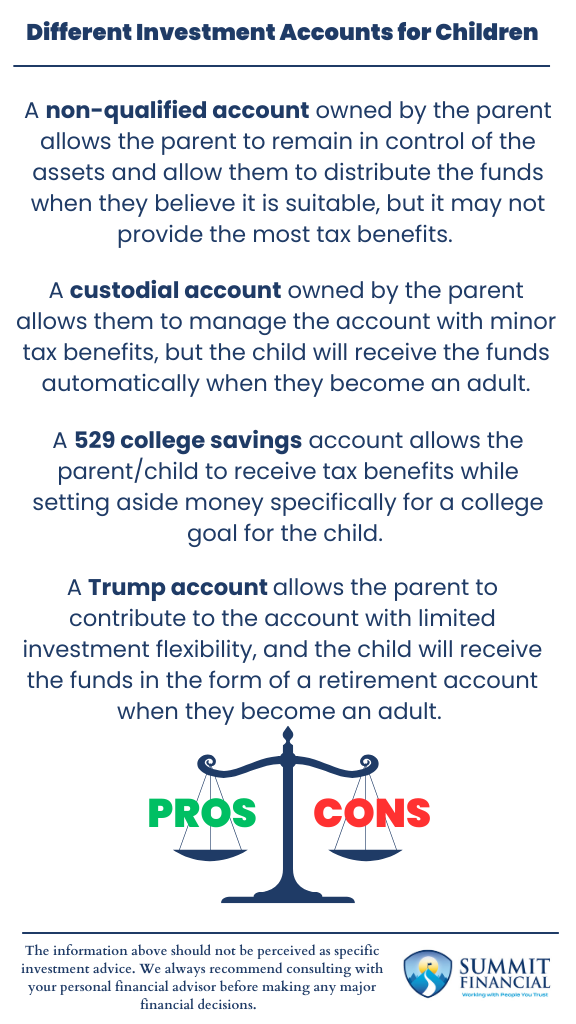

Summary: Different Investment Accounts for Children

- A non-qualified account owned by the parent allows the parent to remain in control of the assets and allow them to distribute the funds when they believe it is suitable, but it may not provide the most tax benefits.

- A custodial account owned by the parent allows them to manage the account with minor tax benefits, but the child will receive the funds automatically when they become an adult.

- A 529 college savings account allows the parent/child to receive tax benefits while setting aside money specifically for a college goal for the child.

- A Trump account allows the parent to contribute to the account with limited investment flexibility, and the child will receive the funds in the form of a retirement account when they become an adult.

Speak With a Trusted Advisor

If you have any questions about your investment portfolio, retirement planning, tax strategies, our 401(k) recommendation service, or other general questions, please give our office a call at (586) 226-2100. Please feel free to forward this commentary to a friend, family member, or co-worker. If you have had any changes to your income, job, family, health insurance, risk tolerance, or your overall financial situation, please give us a call so we can discuss it.

We hope you learned something today. If you have any feedback or suggestions, we would love to hear them.

Sincerely,

Zachary A. Bachner, CFP®

with contributions from Robert Wink, Kenneth Wink, James Wink and James Baldwin

If you found this article helpful, consider reading:

- How Do Bull Markets and Bear Markets Differ

- Navigating College Funding

- Financial Planning Mistakes to Avoid

- Tax Filing Explained

Sources: